Market Analysis: Macroeconomic Factors and the New Risk-Return Dynamic in the Brazilian Stock Market

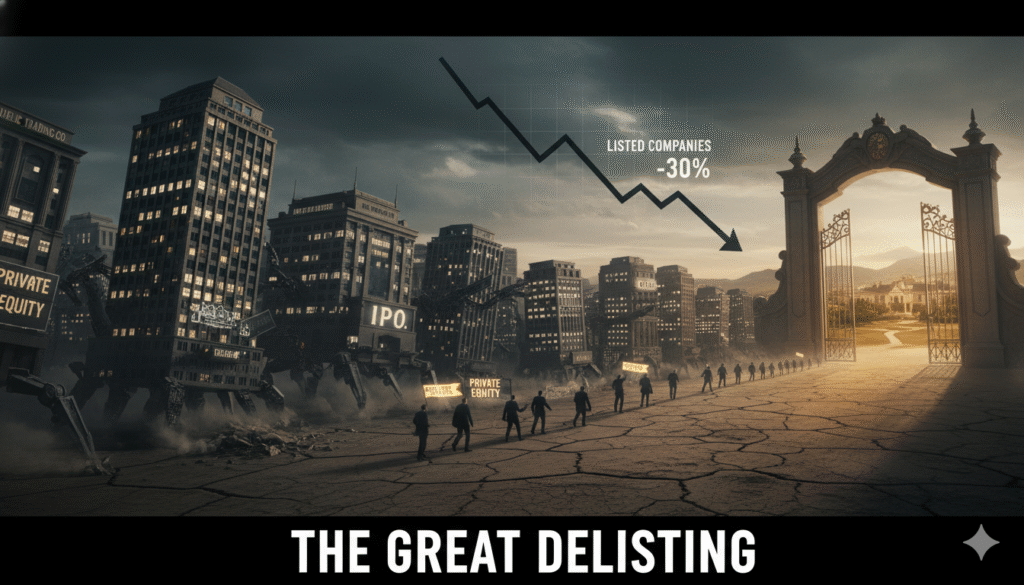

The Brazilian financial market is currently experiencing a notable dichotomy. On one hand, the Ibovespa, the main index of the B3 (Brasil, Bolsa, Balcão), has been on an upward rally, breaking successive records and surpassing the 150,000-point mark. This performance suggests robust investor confidence and a consistent capital inflow, especially foreign capital, attracted by macroeconomic fundamentals and the still attractive valuation of Brazilian blue chips. However, in a contrasting and silent movement, the B3 is witnessing the largest exodus of companies since 2017, with dozens of companies opting to go private. This simultaneous occurrence of records and corporate exits demands a thorough analysis to decipher the true health and the risk-return dynamics of the national stock market.

Development: The Macro Context and Capital Migration

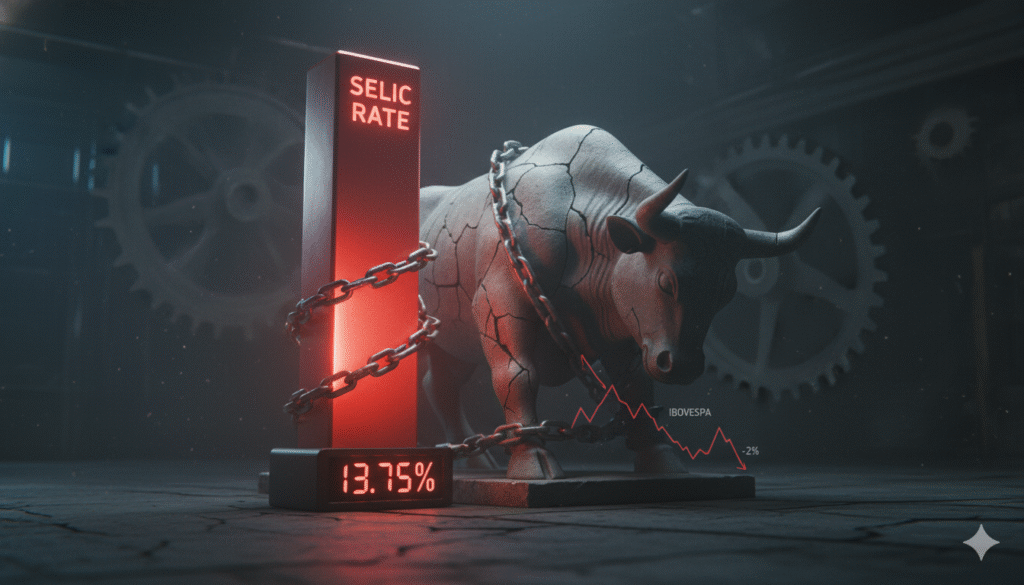

The recent stellar performance of the Ibovespa is primarily driven by highly liquid shares (the so-called blue chips) and foreign capital. The global perception that the Brazilian stock market is “cheap” — with the Price-to-Earnings (P/E) ratio below its historical average, despite nominal records — encourages the flow of international resources. Furthermore, the maintenance of the Selic Rate at restrictive levels (currently at 15%, according to market consensus for the end of 2025) creates a favorable interest rate differential scenario, strengthening the Real and attracting investors seeking carry trade.

However, this same high-interest environment is the main force behind the migration of companies to private ownership. With the Selic Rate at 15%, the cost of raising capital in the equity market for listed companies becomes prohibitive. Fixed Income, with consistent, low-risk returns, directly competes with Variable Income, reducing the liquidity of smaller companies’ shares (small caps) and depressing their stock prices.

For companies, going private becomes an efficiency strategy. By repurchasing their own shares at depressed prices (low valuation), the company spends less to exit the market than the value it might obtain in a share offering (follow-on). The market, by pricing in risk (such as high public debt and the fiscal scenario), is failing to value the growth potential of many of these companies, making the private capital environment more advantageous for management and major shareholders in the medium and long term.

The Impact on B3’s Structure and the Investor’s Perspective

The immediate result of this paradox is a more concentrated B3, where the index (Ibovespa) represents the economy’s diversity less and less. The departure of companies, often smaller and with low liquidity, reduces the universe of opportunities for individual investors and funds dedicated to small/mid caps.

For the investor seeking premium strategies, the reading is clear:

- Capital Concentration: Foreign capital is concentrated in shares with the highest volume and solidity (sectors such as finance, energy, and commodities).

- Attractive Fixed Income: The interest rate differential makes Fixed Income a mandatory allocation, serving as a risk anchor and generating high cash flow.

- Latent Value: The real “gold” in the Brazilian stock market, according to analysts, may lie in high-quality companies that, despite low P/E ratios, show robust profit growth and high Return on Equity (ROE), but require rigorous fundamental analysis and a long-term investment horizon to capture future re-rating.

Conclusion

The current B3 reflects the tensions of the economic cycle: index euphoria contrasted with the cold rationality of the cost of capital. The Ibovespa record is a testament to the resilience of large Brazilian corporations and the attractiveness of the valuation on the global stage, while the exodus of smaller companies is a symptom of restrictive monetary policy and low liquidity for the segment. Premium investors should maintain a posture of strategic discipline, balancing the security of high-interest rates with a careful search for latent value in Variable Income, recognizing that the current dynamic favors extreme selectivity and sophisticated macroeconomic analysis.

Legal Disclaimer: This content is for informational purposes only and does not replace the guidance of qualified professionals.